Is Your Business Ready to Switch from Cash to Accrual Accounting?

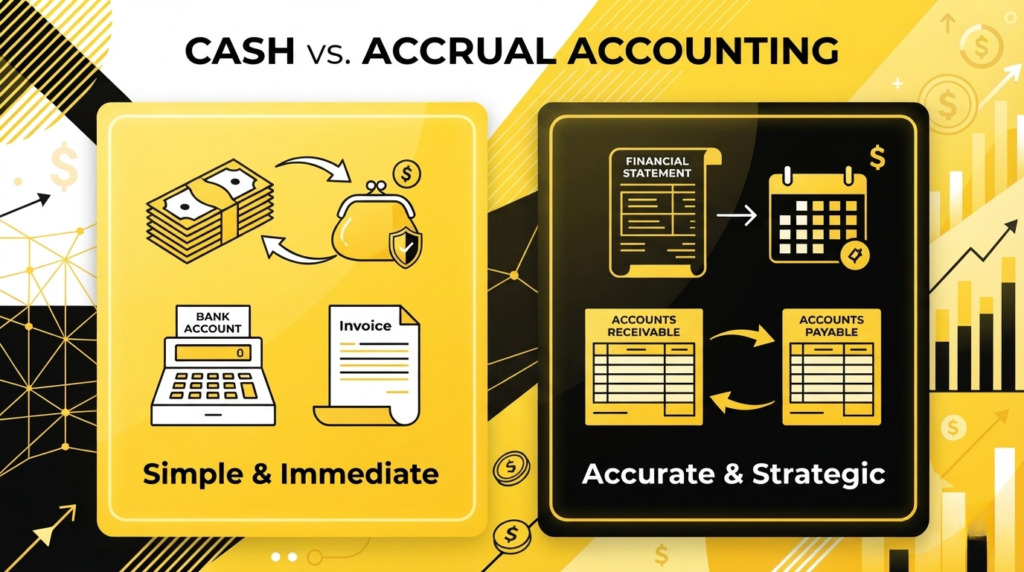

If you’ve ever checked your bank account, felt like things were fine, and then got hit with a bunch of unpaid bills out of nowhere, you’ve already experienced the difference between cash and accrual accounting without knowing it. Most small business owners just pick a method when they’re starting out and never really think about it again. However, what works when your business is small doesn’t always work as things start to grow. So here’s a breakdown of both methods and how to know when it might be time to switch. In simple terms, cash accounting records income and expenses when money actually moves in or out of your account, while accrual accounting records them when they are earned or incurred, regardless of when cash changes hands. The method you use affects your financial statements, your taxes, and in some cases, you may not even get to choose. What Is Cash Accounting? Cash accounting is the method where you record income when money actually comes in and expenses when money actually goes out. If a client pays you in June, that’s June income. If you get a utility bill in June but pay it in July, that’s a July expense. It’s simple, it’s straightforward, and for a lot of small businesses just getting started, it works perfectly. You’re focused on your bank balance, how much is coming in, how much is going out, and cash accounting reflects that directly. What cash accounting does well: Simple to maintain and easy to understand Lower bookkeeping complexity Gives a clear view of actual cash coming in and going out Works well for freelancers and small service businesses with low transaction volume Where it starts to fall short: When you have unpaid invoices or vendor bills, your books don’t tell the full story Hard to do meaningful budgeting or forecasting Bank balance alone can become misleading as the business grows Lenders and investors generally prefer accrual-based financials What Is Accrual Accounting? Accrual accounting records income when it’s earned and expenses when they’re incurred, regardless of when cash actually moves. So if you make a sale in June but the customer has 30 days to pay, that’s still June revenue. And if you receive a utility bill in June but pay it in July, it shows up as a June expense. The result is a much more accurate picture of how your business is actually performing month to month, as June stays in June and July stays in July. You can look back at your financials and see which months were profitable, which were slow, and plan accordingly. What accrual accounting does well: More accurate financial statements as income and expenses match the period they actually belong to Supports budgeting and forecasting based on real trends Stronger reporting for lenders and investors Better insight for strategic decisions at the controller level Makes it possible to track accounts receivable, accounts payable, inventory, and other balance sheet items properly Where it’s more complex: More moving parts and higher bookkeeping complexity Requires understanding of balance sheet accounts, like accounts receivable and accounts payable Takes more time to set up and maintain properly Cash vs Accrual: How They Compare Category Cash Accounting Accrual Accounting Income recorded When cash is received When the sale is made/earned Expenses recorded When cash goes out When an expense is incurred Complexity Simple More complex Best for Small businesses and freelancers Growing businesses, inventory, AR/AP, investors Forecasting/budgeting Limited Strong Lender/investor reporting Less preferred Preferred Accounts receivable/payable Not tracked Tracked on the balance sheet Quickbooks Online Supported Supported Which Industries Tend to Use Each Method? Cash accounting works well for freelancers, consultants, and very small service businesses where transactions are straightforward and volume is low. For example, if you run a small business with 25 transactions a month, cash accounting is probably all you need. Accrual accounting is generally the better fit for construction, manufacturing, retail, e-commerce, healthcare, property management, and any company looking to bring in investors or secure a line of credit. That said, carrying inventory does not automatically mean you have to use accrual accounting. Since the 2017 Tax Cuts and Jobs Act, businesses with average annual gross receipts under the IRS threshold ($32 million for 2026) can use cash accounting even if they carry inventory. Inventory is a strong reason accrual accounting gives you more useful financial information, but it is no longer something that forces the switch for most small businesses. The Biggest Misconception: Profit Doesn’t Equal Cash One of the most common things business owners get wrong is assuming that if the business is profitable, there should be cash in the bank. That’s not always true. A business can be profitable on paper and still have very little cash if customers haven’t paid yet. Under accrual accounting, that $400,000 in accounts receivable shows up as an asset on your balance sheet, but it’s not in your bank account. Cash accounting wouldn’t reflect that sale at all until the money actually arrives. That’s why looking at your financial statements through an accrual lens gives you a much fuller picture of where your business actually stands. How Does This Affect Taxes? The accounting method you choose affects when income and expenses are recognized for tax purposes, which means it can impact your taxable income in a given year. It also affects how useful your financial reports are when filing. One thing worth knowing: QuickBooks Online can run reports using either method, so you can toggle between cash and accrual views. But just changing the report setting doesn’t actually convert your books, as a proper transition from cash to accrual accounting requires cleaning up the balance sheet, including accounts receivable, accounts payable, prepaids, inventory, fixed assets, and accrued expenses. So, When Should You Switch? There’s no one-size-fits-all answer, but here are some clear signs it might be time to move from cash to accrual accounting: You have customers who pay on net 30 or net 60 terms You have vendor bills

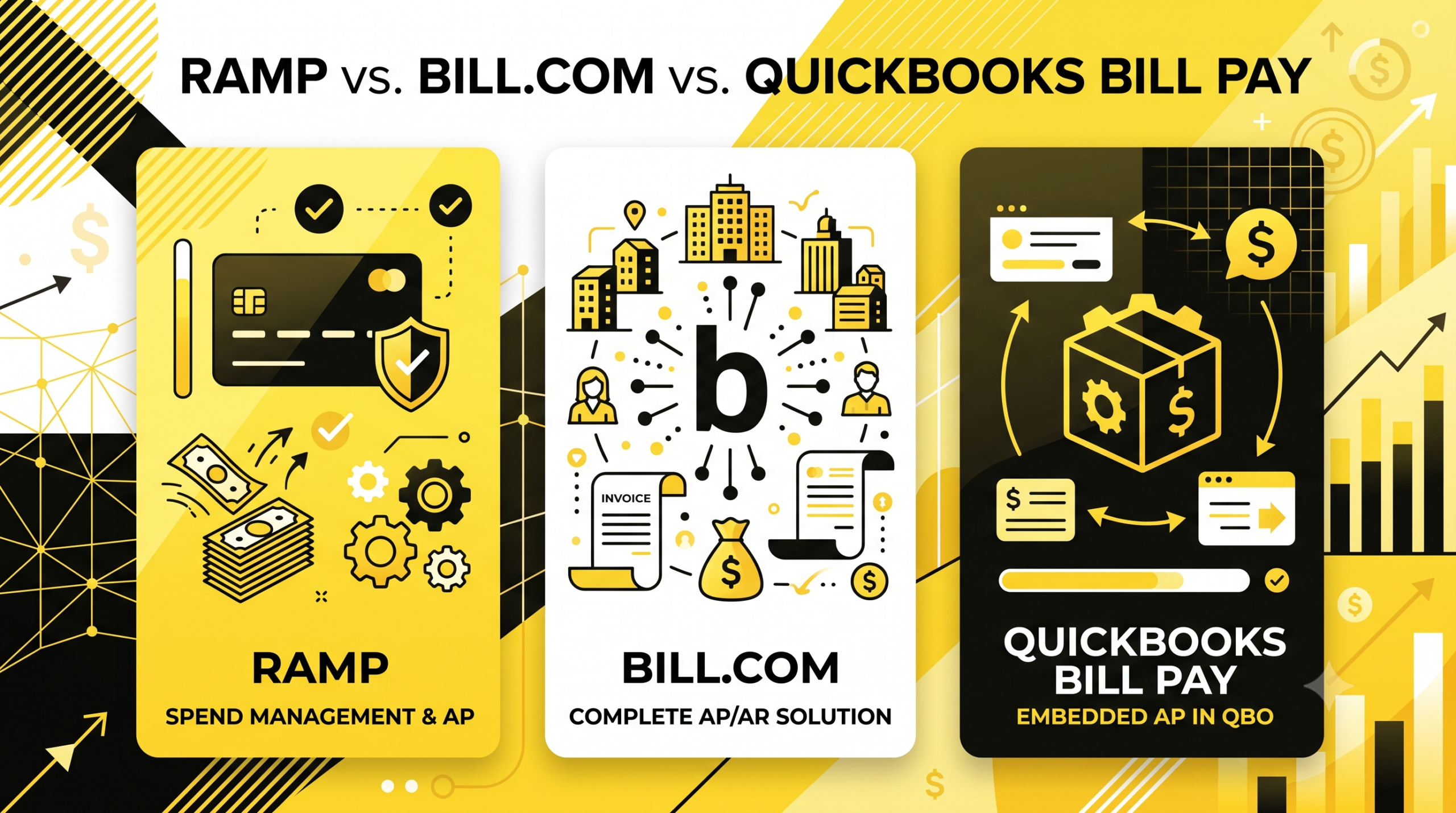

Ramp vs Bill.com vs QuickBooks Bill Pay: AP Tool Comparison

Let’s be honest, dealing with vendor invoices is nobody’s favorite part of running a business. You get a PDF, you enter it manually, you chase someone for approval, and then you’re not even sure if the payment went out. Multiply that by twenty vendors, and it becomes a real problem. The three most popular ones are Ramp, Bill.com, and QuickBooks Bill Pay. They all solve the same basic problem, but they’re built a little differently and for slightly different types of businesses. What is AP automation? Accounts payable is just the money your business owes to vendors, and someone has to make sure that money actually gets to them. In practice it means a lot of manual invoice entry, a lot of approval follow-ups, and a lot of double-checking that payments went through. AP automation takes that whole process and puts most of it on autopilot. Ramp Ramp started out as a corporate card company back in 2019 and has grown into something much bigger. Now it handles AP automation, expense management, and corporate cards all in one place. Cards, expenses, bill payments, and banking all exist in one platform. The way it works: you or your vendor uploads an invoice PDF, and Ramp reads it automatically — vendor name, amount, invoice number, all of it. From there you set up who needs to approve it, when it gets paid, and it all syncs back to QuickBooks or Xero without you doing anything extra. Ramp also does automated receipt matching, real-time spend controls, and policy enforcement that runs in the background. One thing worth knowing: Ramp’s free tier already includes automatic QuickBooks and Xero sync. Bill.com doesn’t give you that until you’re on a higher paid plan, which is a meaningful difference if you’re watching your budget. On pricing, the base plan is free and the Plus plan runs $15/user/month whereas the Enterprise plan is custom. For Bill Pay specifically, Ramp charges $0.59 per ACH transaction and $1.99 per check as of June 2026, though those fees get waived if you’re paying from a Ramp Business Account. The main thing Ramp doesn’t do is AR, so if you also need to send invoices and collect money from customers, you’ll need something else for that service. What Ramp does well: Free tier with genuine AP automation, corporate cards, and expense management Automatic QuickBooks and Xero sync on the free tier Real-time spend controls and receipt matching Integrates with NetSuite, Sage Intacct, QuickBooks, Xero, and 50+ other tools ACH and check payments, domestic wires, and international payments Where it falls short: No AR functionality — you’ll need a separate tool to invoice clients and collect payments Advanced approval workflows and multi-entity support are locked behind paid tiers Primary fit is US-based businesses with a US bank account Bill.com Bill.com (now officially just “BILL”) has been around longer and is one of the most widely adopted AP/AR platforms for small and mid-market businesses. The big difference from Ramp is that it handles both AP and AR, so you can manage what you owe and what you’re owed all in one place. The AP side works similarly, vendors send invoices, the system pulls the details using AI-powered data extraction, you approve and schedule payment. It integrates directly with QuickBooks Online, QuickBooks Enterprise, Xero, Sage Intacct, Oracle NetSuite, and Microsoft Dynamics, with sync running automatically or on-demand. Bill.com’s vendor network is one of its strongest selling points. With over 8 million businesses in its network, paying a new vendor often means they’re already on the platform and you don’t need to collect bank details manually. The platform also processes around 1% of US GDP annually, which gives a sense of the scale. Bill.com claims customers save around 50% of their time on AP processes. That’s their own reported figure, but it lines up with what you’d expect when you eliminate manual data entry and email approval chains. On pricing, the Essentials plan starts at $49/user/month, Team at $65/user/month, Corporate at $89/user/month and the Enterprise plan is custom. Transaction fees also apply on top of the subscription depending on payment method. One thing to note is that automatic QuickBooks sync isn’t available on the base Essentials plan, you have to be on the Team tier or above for that. What Bill.com does well: Handles both AP and AR in one platform Network of 8+ million businesses for faster vendor payments Native two-way sync with QuickBooks, Xero, NetSuite, Sage Intacct, and Microsoft Dynamics AI-powered invoice capture with 95% day-one accuracy on key fields Duplicate invoice detection before payment Dedicated accountant dashboard for firms managing multiple clients Where it falls short: Costs add up quickly with users and transaction volume QuickBooks automatic sync requires Team tier or above Approval workflow customization is limited for complex hierarchies or multi-entity structures QuickBooks Bill Pay QuickBooks Bill Pay isn’t a separate product as it’s built right into QuickBooks Online. Which is honestly its whole selling point. You’re already in QBO to do your books, so being able to pay bills from the same place without logging into anything else is genuinely convenient. You can create bills, get approvals, and send payments via ACH or check without leaving QBO. And as of June 2026, Intuit updated their pricing so that all Bill Pay tiers now include standard ACH with no per-transaction fees which makes it an even more attractive option for smaller operations that don’t want to pay per payment. The tradeoff is automation depth. QuickBooks Bill Pay requires more manual data entry than dedicated AP platforms and doesn’t have the same depth of approval workflows or vendor network. For a business processing a handful of vendor bills each month, that’s totally manageable. For a business with a high volume of invoices coming in constantly, it’ll start to feel like a barrier. What QuickBooks Bill Pay does well: Everything stays in one system — no separate login or platform No learning curve if you’re already on QuickBooks $0 ACH transaction fees

The Role of a Controller — What They Do and When Your Business Needs One

There is a certain stage in a growing business where having someone enter transactions is no longer enough. The books are getting done, but nobody is analyzing them. Nobody is catching the trends, flagging the variances, or making sure the financial statements actually reflect what is happening. That is not a bookkeeping problem. That is a controller problem. What Is a Controller? A controller is a senior accounting professional who makes sure the financial information coming out of your business is accurate, reliable, and actually tells you how the business is doing, whether that is you as the owner making decisions about growth, a bank reviewing your financials before approving a loan, or an investor trying to understand where things stand. Someone has to be responsible for making sure those numbers are right before they land in front of people who are going to act on them. That is the controller’s job. They are not doing the day-to-day transaction work. Your bookkeeper and junior accountants handle that. The controller is the person making sure all of that work adds up to something accurate and reliable. How the Accounting Team Fits Together Picture a pyramid. At the bottom, bookkeepers and junior accountants handle the transactions — entering invoices, recording payments, and categorizing expenses. Above them, an accounting manager reviews that work and makes sure it is complete. At the top sits the controller, reviewing the full financial picture at month-end and making sure the numbers actually make sense. For larger payments, the controller is often the one who reviews and approves before anything goes out. Month-end is where a controller really earns their place. Rather than just checking that transactions were entered, they go through the financial statements looking for anything that seems off – an account balance that jumped compared to last month, an expense that looks higher than usual, a revenue figure that does not match what was expected. It is not about auditing every single line. It is about knowing what normal looks like for that business and catching anything that does not fit before it becomes a real problem. Controller vs. Bookkeeper — What Is the Real Difference? A bookkeeper is focused on keeping up with transactions as they happen — entering the data, making sure invoices are recorded, and reconciling accounts. It is detailed, necessary work, but it is mostly transactional. A controller is focused on what those transactions mean once they are all in. They are analyzing trends, reviewing whether accounts are properly categorized, checking that accruals and prepaids are handled correctly, and making sure the financial statements paint an accurate picture of the business. It requires a different level of experience and a different mindset — less about recording what happened, more about understanding what it means. What a Controller Actually Does Each Month Beyond the high-level oversight, controllers are involved in specific and consequential work every month: Reviewing financial statements line by line for unusual activity Verifying that recurring items like prepaid expenses and accruals are properly accounted for Troubleshooting when something does not reconcile – a bank statement that is off, a journal entry posted to the wrong account, a vendor set up incorrectly Approving significant outgoing payments before they are processed Making sure everything balances before financials go to the owner, a lender, or an investor That last point matters more than most business owners realize. The financial statements a controller signs off on are the ones that get used to make real decisions. A Real Example: What Controller-Level Oversight Changed for a Seafarer Client When Seafarer took on a precision medicine company as a client, the books needed significant work. The previous accounting team had left journal entries incorrect, reconciliations incomplete, and financial statements that gave the owner no real visibility into how the business was performing. Seafarer’s controller reviewed everything from the ground up, identified what needed to be corrected going back into 2024, and worked with the accounting manager to get it done. One of the more impactful changes involved payroll. Instead of recording all wages in a single expense line, the controller created separate accounts for administrative payroll, warehouse payroll, and purchasing payroll — and moved the appropriate portions into cost of goods sold. That one change gave the owner a much clearer picture of where money was actually being spent and what it was producing. By the time the cleanup was complete, the owner had financial statements he could stand behind — and was able to approach a bank for a line of credit with confidence. That is what controller- level oversight makes possible. Does Every Small Business Need a Controller? Not at every stage – but every business reaches a point where having someone who can interpret the financial statements becomes essential. Every owner wants to know the same things: is the business actually making money, can it afford to grow, and is adding a new service or product a smart move right now? Those are not questions a bookkeeper can answer. They require someone who can sit down with the financials, understand what they are showing, and translate that into something the owner can act on. Without that, decisions get made on instinct rather than data — and that is where things tend to go wrong when the stakes are high. According to a U.S. Bank study, 82% of small business failures are caused by cash flow problems, not a lack of profitability. A controller who is actively reviewing your financials and flagging issues early is one of the most direct ways to prevent that outcome. Signs It Might Be Time to Bring in a Controller Use this as a self-diagnostic. If any of these apply, it is worth having a conversation: Your financials are being produced, but nobody is analyzing them. Numbers come in each month, but no one is reviewing trends, flagging variances, or connecting the data to the decisions being made. Volume has outgrown your current team. Things that used

Accounts Payable and Accounts Receivable: What They Are and Why They Matter

Revenue looks fine, invoices are going out, but there’s never quite enough cash when it’s needed. Sound familiar? This is one of the most common situations small business owners find themselves in, and most of the time, it has nothing to do with how well the business is actually doing. It comes down to how accounts payable and receivable are being managed, and getting that wrong affects everything from payroll to vendor relationships to the decisions you make every day about your business. What Are Accounts Payable and Accounts Receivable? Accounts payable is the money your business owes for goods or services already received. Accounts receivable is the money your customers owe you. They are two sides of the same transaction. To understand these terms, let’s take the example of a small retail business. The store owner buys various products from a supplier but does not pay for them right away; instead, both individuals agree that payment will be made within 30 days. The store receives the products, sells them, and generates revenue, but until the supplier is paid, that outstanding amount is recorded on the books as accounts payable. On the other hand, the supplier that delivered the goods but has not been paid yet, for them, that outstanding amount is accounts receivable. It is the money they have already made but have not yet collected. How do Accounts Payable and Accounts Receivable Work Together? Businesses that succeed know how to balance both. If your customers have 30 days to pay you, but you must pay your supplier in 15 days, your money is going out before it comes in. Keeping your accounts receivable terms shorter than your accounts payable terms means you collect from customers before your own payments are due, and that leads to positive cash flow. The Cost of Ignoring AP and AR When AP and AR are not handled properly, the day-to-day processes essential for running your business are affected. A supplier puts you on prepayment terms because your account has been consistently late. You start drawing on a credit line to cover payroll, not because the business is struggling, but because a large amount in receivables is sitting uncollected. You delay a vendor payment, hoping a client pays first, and they do not. According to QuickBooks’ 2025 Small Business Late Payments Report, 56% of US small businesses are currently owed money from unpaid invoices, averaging $17,500 per business. And according to Kaplan Collection Agency, 55% of all B2B invoiced sales in the US are past due. That is not just a cash flow issue. It is a collection problem that most businesses are not actively managing. According to Monite, 54% of SMEs regularly pay their own bills late — often not because they don’t have the money, but because AR delays mean the cash isn’t available when AP comes due. Without proper accrual accounting, your financial reports will not reflect any of this accurately. A business can look profitable on paper while running out of usable cash underneath. When You Should Get Help? Here are the signs that it is time to get help. Your invoices are aging past 60 days with no follow-up process in place. You have no real visibility into what your cash position will look like 45 days from now. You are making hiring or vendor decisions without knowing if the cash will actually be there. According to CashinUSA’s 2025 report, 65% of businesses spend roughly 14 hours per week chasing overdue invoices. That is time that should be going into running the business, not managing unpaid bills. How Seafarer Can Help If you are making financial decisions without a clear picture of your cash position, that is exactly what we are here for. At Seafarer Consulting, we have seen firsthand what happens when AP and AR go unmanaged. We have helped clients recover long-overdue invoices that customers simply were not going to pay until someone followed up. We have also helped businesses avoid unnecessary late fees just by making sure supplier invoices were paid on time and nothing slipped through the cracks. Book a free consultation with us at seafarerconsulting.com, and let’s take a look together.

What a Fractional CFO Actually Does in the First 90 Days

There’s a common misconception about what hiring a Fractional CFO actually means. Many business owners imagine high-level strategy sessions and sweeping financial decisions from day one. In reality, the process is different and can be even more valuable. During the first 90 days, the main goal is to build a solid financial foundation. Before making plans, a Fractional CFO needs to understand the business’s current situation. They need to look at the numbers, find where the gaps are, and get systems in place to help guide the decisions down the road. Here’s what that process actually looks like, phase by phase. Days 1–30: Getting a Clear Picture The first month is about assessment. A Fractional CFO’s job in this phase is to get an honest, neutral look of the business that includes analyzing financial statements, figuring out where the cash is going, and seeing what’s working and what isn’t. This is also when the books get cleaned up. If things aren’t being reconciled or the reporting is inconsistent, that gets flagged immediately. It’s impossible to make good predictions if the data is a mess, so fixing the books is almost always the first item on the list. Along with the financial review, a good fractional CFO is going to ask a lot of questions. What are the actual business goals? Which decisions feel the hardest right now? Where do you feel the most exposed? Those answers are basically the roadmap for everything else. Days 31–60: Building the Systems Once the CFO examines all the key details, you can then move to building the financial infrastructure that allows you to make better financial decisions everyday. Cash flow forecasting is usually one of the big priorities here. Most small businesses don’t have a reliable way to see where their cash will be in 60 or 90 days. A CFO builds that visibility. Instead of just reacting when cash gets tight, the business can see it coming and actually manage it. Budgeting is the next step. If the business is flying blind or using a budget that hasn’t been touched in months, this is when a real one gets built. A budget isn’t just a document; it’s an accountability tool that warns you when things are heading off track. KPI tracking is another key outcome in this phase. Revenue doesn’t tell the whole story. Depending on the industry, the metrics that actually matter might be gross margins, what it costs to get a new customer, or how long it takes for invoices to get paid. A CFO figures out which numbers are the ones to watch and sets up a way to track them consistently. Financial modeling is the last step of this phase. Financial modeling is the last part of this phase. Whether you’re thinking about a new hire, changing your prices, or expanding, a model lets you test those ideas before you commit to them. Most small businesses just don’t have the internal capacity to do this kind of analysis on their own. Days 61–90: From Insight to Action By month three, the foundation is in place. The goal of the Fractional CFO is to use the systems that were built earlier to translate data into decisions. If the first month showed a gap in cash flow, this is when the plan to fix it gets put into motion. If the analysis showed a service that isn’t performing well or a way to get better margins, those changes happen now. Strategy sessions start looking further ahead—thinking about expanding, new services, or pricing shifts. This is also when reporting becomes a routine. Instead of scrambling for numbers before a big meeting, the business has a clean monthly financial package that tells the story clearly. By day 90, the business owner finally understands the numbers and trusts the data. Most importantly, they have a clear plan they can actually act on. Is a Fractional CFO Right for Your Business? If you’re making big decisions without reliable financial data behind them, that’s your answer. At Seafarer Consulting, our Fractional CFO engagements are built around what your business actually needs — no full-time commitment, no one-size-fits-all approach. Just the right level of financial leadership at the right time. Want to talk through what this could look like for your business? Contact us today and let’s discuss how we can support your business’s financial growth.

Why Many Small Businesses Start Outsourcing Their Accounting in March

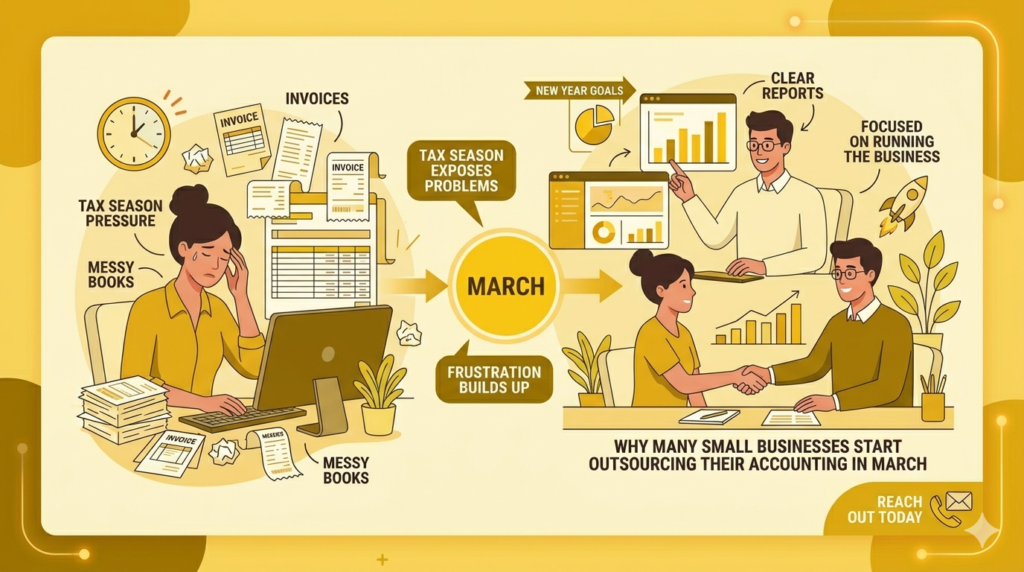

For a lot of small business owners, the decision to outsource accounting does not happen randomly. It tends to build up over time, and for many, March is when everything finally clicks. It is usually a mix of tax season pressure, growing workload, and realizing the numbers are not as clear as they should be. 1. Tax season exposes the problems By March, most business owners are already deep into tax prep. This is usually when issues show up. Books are messy, transactions are unclear, or numbers do not match. What felt “good enough” all year suddenly is not. 2. New year goals start to feel real January is all about planning. February still feels early. But by March, people start asking real questions. Are we actually making money? Can we afford to grow? If the numbers are not clear, those questions are hard to answer. 3. Time gets tighter Business picks up after the holidays. Owners get busy again and accounting keeps getting pushed aside. What used to be manageable becomes something they avoid. 4. DIY accounting stops working A lot of small business owners try to do their own books at first. Spreadsheets and basic tools can work early on, but as things grow, it gets more complicated. More transactions, more moving parts. By March, many realize they cannot keep up. 5. Frustration builds up Tax season stress, messy records, and unclear numbers all hit at once. It becomes less about saving money and more about reducing stress. 6. Outsourcing starts to make sense At this point, outsourcing feels like a relief. Instead of guessing, they get clear reports and someone handling the details. It frees them up to focus on running the business. 7. It is the right time to fix things March is still early in the year. Cleaning up books now means the rest of the year can be based on accurate data. Waiting until year-end usually just repeats the same problems. At the end of the day, March is when everything clicks. Tax season highlights the issues, goals create pressure, and workload makes it clear something needs to change. If you are starting to feel that pressure, this is usually the point where having the right support makes a big difference. We work with small businesses to clean up books, handle monthly accounting, and give clear visibility into cash flow so you can make better decisions without the stress. If you want to get ahead of it before the year gets away from you, reach out and we can take a look together.

The Q1 Financial Checkup Every Small Business Should Do

Three months in, you have real data — not projections, not hope. Here’s how to use it. A client came to us last April convinced their business was doing fine. Revenue “seemed okay,” expenses felt normal, and they hadn’t looked at the books since January. By the time we pulled everything together, they’d missed a window to catch a cash shortfall early, one that a simple Q1 review would have flagged in February. This is more common than most business owners realize. The first quarter ends quietly, and most people are too busy running the business to stop and look at how it’s actually doing. But that first look , when you’ve got three full months of real numbers, is one of the most valuable financial moments of the year. Here are the five areas worth reviewing right now: Revenue: Is the year actually starting the way you planned? Pull your Q1 revenue and put it next to your original forecast. Not to judge yourself — but to understand what’s true. Is revenue tracking ahead, behind, or roughly on pace? Are sales growing month over month, or did January outperform and March slow down? If you’re behind, March is the right time to adjust, not June. A small gap in Q1 is manageable. The same gap ignored through Q2 is a problem. Expenses: What’s actually eating into your margin? Expenses have a way of expanding without anyone noticing. The first quarter tends to pile on costs: annual renewals, new hires, early-year vendor price increases. Scan through your spending by category and ask: Does this match what I budgeted? Is anything higher than expected? Common things we spot in Q1 reviews: software subscriptions nobody’s using, marketing spend that quietly doubled, payroll costs higher than projected because of timing. None of these are emergencies on their own, but catching them now means you have nine months to adjust. Cash Flow: Profit doesn’t pay the bills, cash does A profitable business can still run into serious trouble if cash isn’t moving through fast enough. Look at your current bank balances, what’s outstanding from customers, and any large payments coming up in Q2. If you’re noticing that customers are paying slower than last year, that’s worth addressing now. Tightening up your invoicing process or revisiting payment terms in March has a compounding benefit for the rest of the year. Wait until fall and you’re just managing symptoms. Your Balance Sheet: The story behind the story Most business owners live in their P&L and barely glance at the balance sheet. That’s understandable, but it means they’re often missing what’s building underneath. Take a few minutes to look at your loan balances, inventory levels, and overall equity. Is your financial position getting stronger or weaker compared to where you were at the start of the year? These numbers give you a clearer picture of the business’s actual health, not just its recent activity. Your Forecast: Update it while it still mattersYour January projections were based on assumptions. Now you have data. Use it.Updating your forecast in March, by adjusting for what Q1 actually showed, helps you make better decisions about hiring, spending, and growth for the rest of the year. It also means you’re not operating on stale assumptions when Q3 planning comes around. Why This Is Worth 30 Minutes of Your Time A Q1 checkup isn’t about having perfect numbers or catching every problem. It’s about staying oriented. The businesses we work with that review their financials regularly, even briefly, respond faster, plan better, and rarely get blindsided at year-end. The businesses that wait until December to look at January almost always find something they wish they’d caught earlier. If you want help running through your Q1 numbers, or if your books aren’t quite in shape for a review like t, that’s exactly what we do. Reach out and we’ll set up a time to take a look together.

Turning Tax Changes Into Opportunities

You may have heard the phrase “Big Beautiful Bill” used to describe large tax reform laws. The name may sound informal, but it has a significant impact. If you know what to look for, this “BBB” can significantly alter your tax situation and typically result in significant financial opportunities. Its main objectives are to increase the amount of money in the hands of taxpayers, promote growth, and simplify the tax system. Keep reading to know how changes like these can affect you and where the savings often show up. 1. Wider Brackets and Lower Tax Rates Lower tax rates are among the most obvious effects of significant tax reform, frequently paired with updated income brackets. Now, this means that a lot of individuals would see an overall lower tax bill and this is especially true for middle-income earners. Business owners may also benefit from reduced taxes on profits and have more take-home pay and stronger cash flow. When rates shift, timing starts to matter more. Decisions around bonuses, distributions, and when income is recognized can make a real difference. 2. Bigger Deductions for Businesses Large tax bills frequently attempt to encourage investment by increasing the generosity of deductions. This may entail treating startup and operating costs more favorably, raising the deduction limit for small businesses, or writing off technology and equipment earlier. The benefit is straightforward. Businesses can reduce their taxable income in the year they spend the money if they plan ahead. 3. Advantages for specific kinds of business owners Tax reform frequently contains provisions specifically targeted at you if you are the owner of an LLC, S-corp, or partnership. This could have the following benefits: Deductions based on eligible business income A reduced tax burden without altering the structure of your company Better outcomes when profit splits and compensation are carefully planned This is one thing you should pay close attention to. Small adjustments can lead to meaningful savings, while missed rules can limit the benefit. 4. Higher Standard Deductions and Easier Filing One more goal of tax reform is simplification. A lot of taxpayers benefit from higher standard deductions, which reduces the need to itemize. This helps because: Less paperwork and record-keeping Lower preparation costs More predictable tax outcomes each year For many households, this means keeping more cash without having to jump through hoops. 5. Incentives for Hiring and Growth Major tax changes often include credits and relief tied to expanding a business. These can show up as: Hiring incentives Payroll-related relief Credits for investing or innovating locally These benefits are easy to overlook, but they can add up quickly for companies that are growing or adding staff. 6. Planning Still Makes the Difference A common mistake is assuming tax savings happen automatically. In reality, the biggest wins usually go to those who take time to adjust their approach. That often includes: Reviewing how the business is structured Rethinking how owners are paid Being intentional about when income and expenses hit Aligning tax decisions with long-term goals Without a plan, many of the built-in opportunities simply get missed. Whether it’s casually called a “Big Beautiful Bill” or officially labeled tax reform, these laws can open the door to real savings. The key is understanding how the changes apply to your specific situation. For business owners and individuals, this is less about politics and more about strategy. The rules may shift, but the objective stays the same: keep more of what you earn while staying compliant. If you are unsure how recent or upcoming changes affect you, it is worth reviewing your setup now. Waiting too long often means leaving money on the table. If you’re not sure how these changes translate to your own numbers, we can help walk through your current setup and highlight where savings may exist, if any adjustments make sense.

How Finance BPO Services Support Small and Medium-Sized Enterprises (SMEs)

In these evolving times, especially when it comes to business trends, small and medium-sized enterprises (SMEs) face numerous challenges. This can range from managing operational costs to staying compliant with changing regulations. However, one of the most significant challenges that an SME can experience is handling complex financial operations without draining resources. This is where Finance Business Process Outsourcing (BPO) services come into play. Below, we explore the benefits of finance BPO services for SMEs and how these services can be a gamechanger for your business. Access to Expert Resources One of the most note-worthy advantages of finance BPO services is the access they provide to a group of financial experts and professionals. SMEs often operate with limited resources, making it challenging to hire and maintain a full-time finance department. Finance BPOs can solve this issue by offering the expertise of highly qualified professionals, ensuring that SMEs’ financial operations are in skilled hands. This setup not only enhances the quality of financial management but also provides SMEs with advisory services that can guide strategic decision-making. Cost Efficiency Operating under the constant pressure to minimize costs, SMEs find finance BPO services to be a cost-effective solution. By outsourcing finance functions, businesses can convert fixed costs into variable costs, paying only for the services they require. This flexibility allows SMEs to allocate resources more efficiently and avoid the overhead associated with hiring in-house staff, such as salaries, benefits, and training expenses. Moreover, finance BPO providers benefit from economies of scale, which can translate into lower costs for their clients. Enhanced Focus on Core Business Outsourcing finance functions enables SMEs to redirect their focus and resources towards core business activities that drive growth and innovation. With the assurance that financial operations are managed by experts, business owners can concentrate on developing new products, expanding into new markets, and enhancing customer service. This strategic focus is crucial for staying competitive and achieving long-term success. Scalability and Flexibility As SMEs grow, their financial operations become more complex and voluminous. Finance BPO services offer scalability, allowing businesses to adjust the level of services based on their changing needs. Whether it’s managing an increase in transactions, expanding into new countries with different compliance requirements, or requiring more sophisticated financial analysis, finance BPO providers can tailor their services accordingly. This flexibility supports SMEs through various stages of growth without the need to continually invest in new financial management software or hire additional staff. In conclusion, for small and medium-sized enterprises, finance BPO services are not just a means to reduce costs; they are a strategic partnership that can propel businesses forward. By providing access to expert resources, enhancing cost efficiency, allowing a sharper focus on core activities, offering scalability, and unlocking advanced technologies, finance BPO services equip SMEs with the capabilities to navigate the complexities of today’s business environment successfully. In embracing these services, SMEs can ensure their financial operations are robust, compliant, and aligned with their growth ambitions, setting a solid foundation for sustained success.

Leveraging Outsourced CFO Services for Strategic Financial Leadership

Nowadays, companies need robust financial leadership to navigate complex challenges and seize growth opportunities. However, not all businesses, especially small and medium-sized enterprises (SMEs), can afford or justify a full-time Chief Financial Officer (CFO). This is where outsourced CFO services come into play, offering strategic financial leadership without the overhead costs of a full-time executive. This blog explores the benefits of leveraging outsourced CFO services to enhance your business’s financial strategy and overall success. The Role of an Outsourced CFO An outsourced CFO provides high-level financial expertise on a flexible, part-time, or project-based basis. These seasoned professionals bring a wealth of experience and insights, offering services that range from financial planning and analysis to risk management and strategic planning. The first key function of a CFO is Strategic Financial Planning. They are needed in developing long-term financial strategies aligned with business goals. Next, Financial Reporting and Analysis. CFOs are great in providing accurate and timely financial reports to guide decision-making. Third, Cash Flow Management. CFOs ensure that the company has optimal cash flow to support business operations and growth. Fourth, Risk Management. These professionals are experts in identifying and mitigating financial risks. Lastly, Budgeting and Forecasting. They are skilled in creating realistic budgets and forecasts to guide business planning. Now, let us discuss the benefits of outsourced CFO services: Cost-Effective Expertise – Hiring a full-time CFO can be costly, particularly for SMEs. Outsourced CFO services offer access to top-tier financial expertise at a fraction of the cost. Businesses can tailor the level of service to their specific needs and budget, ensuring cost-effective financial leadership. Enhanced Strategic Planning – Outsourced CFOs bring a strategic perspective to financial management. They work closely with business leaders to develop and implement financial strategies that drive growth, improve profitability, and enhance overall business performance. Improved Financial Reporting and Analysis – Accurate financial reporting and insightful analysis are crucial for informed decision-making. Outsourced CFOs ensure that businesses have access to timely and precise financial data, enabling leaders to make well-informed decisions and respond quickly to changing market conditions. Scalability and Flexibility – One of the significant advantages of outsourced CFO services is their scalability. Businesses can easily scale the level of CFO support up or down based on their needs, whether it’s during a period of rapid growth, a merger, or a financial restructuring. Risk Management and Compliance – Outsourced CFOs play a critical role in identifying and managing financial risks. They ensure that businesses comply with relevant regulations and implement robust risk management strategies to safeguard the company’s financial health. Focus on Core Business Activities – By handling complex financial tasks, outsourced CFOs allow business leaders to focus on core activities such as product development, marketing, and customer service. This leads to improved operational efficiency and business growth. Given the importance of a CFO to your company, the question is, how do you choose the right outsourced CFO service? Selecting the right outsourced CFO service is crucial for maximizing the benefits. Consider the following factors when choosing a provider: Experience and Expertise: Look for CFOs with experience in your industry and a proven track record of success. Reputation and References: Check references and reviews to ensure the provider has a strong reputation for quality service. Customization and Flexibility: Ensure the provider offers customizable services that can adapt to your business’s unique needs. Communication and Collaboration: Choose a CFO who communicates effectively and collaborates well with your existing team. Outsourced CFO services offer a powerful solution for businesses seeking strategic financial leadership without the costs of a full-time executive. By leveraging the expertise of an outsourced CFO, companies can enhance their financial strategy, improve decision-making, and achieve sustainable growth. Embracing this flexible and cost-effective approach to financial management positions businesses for long-term success in an increasingly competitive marketplace.